Buyouts

Last week, one of White Brook’s core holdings, PetIQ (PETQ) accepted a buyout offer by a private equity firm, Bansk Group, at a ~50% premium to the price the day before. We had entered the stock earlier this year, and remarked upon the thesis in our 1Q letter. The IRR on our investment was very good, and while I envisioned a higher price for the stock over time, that price would have taken more time. I’m happy with the outcome.

I thought for this insight I’d highlight three other interesting positions we have that I think are conducive to takeout in the near term, particularly as interest rates show signs of a modest decline and the lending environment is more conducive to buyers.

Green Plains (GPRE) has been a terrible investment for White Brook Capital. There are reasons for the stock’s decline, and reasons that I believe, in other hands, our base case could still be achieved, but those are academic at this point. Today, Green Plains is midway through a standstill agreement with one of their activist investors, Ancora Holdings. The standstill agreement bound Ancora from pursuing a proxy challenge until early 2025 and amassing a greater position in the Company in return for giving the Company one more year to operate as long as it simultaneously pursued strategic alternatives.

Today, Ancora, and virtually all investors are down from their entry price even though the assets of the company continue to be as or more strategic than ever. In February 2025, Ancora will be free to pursue a proxy contest. They will win.

The Company knows this and with this year’s stock performance not as hoped for, they can either make a real effort to sell the Company or lose an embarrassing proxy contest. On their 2Q earnings call they took the uncommon but not unique step of announcing the specific bank and legal counsel they’d hired to try to convince shareholders that this time they are indeed serious about selling the company. They also announced the sale of a small rail terminal asset, outside of that process, and that they’d be using the proceeds to retire high priced debt.

To White Brook, this was a critically important piece of news. Expensive debt, usually not only comes with a higher interest rate to compensate the loaner for the risk of loaning money, but with restrictive debt covenants. Those covenants ensure that the debtor, in a last ditch effort to preserve value for itself, doesn’t move the asset into another corporate structure without paying the debt.

A further reading of the company’s filings confirmed the intuition. The debt holders had a perfected first lien claim to assets that complicated any transfer of the assets and therefore the sale of the Company. The Street overlooked the importance of the words and the development.

Charitably said, it also revealed that initially management was less than serious about pursuing strategic alternatives as this debt would complicate a potential transaction. The passage of time, the Company’s flailing stock price, and Ancora’s provisions in the standstill agreement took the decision out of their hands and the management and board are looking at either being dismissed in embarrassing fashion or selling the Company before the likely proxy contest next year.

Finally, I knew a member of the review committee in a previous life and think she’s a good analyst, an honest broker, and I was heartened to learn she was a key member of the strategic review committee. I think the board will choose to sell the Company and we will at least recover a portion of our to date loss - if there’s a healthy and competitive auction process as we believe there should be, there’s a likelihood we could do better than that.

Afya, LTD (AFYA) has the scent of a John Malone investment in his heyday but perhaps with a family with an even better record of value creation. Unlike the previous two examples where there was or will be a strategic review process. Afya is slowly being taken out in the public markets by a large shareholder that already owns a stable of private companies.

A core principle of finance is that a dollar today is worth more than a dollar tomorrow. We’re all perhaps better acquainted with that axiom today, than several years ago. The Bertelessman family has been gifted the ability to take out Afya slowly south of $20 a share, until it has to entice its final shareholders (in this case us) to sell the remainder at a healthy premium. Public shareholders have yet to punish them for pursuing this approach by refusing to sell shares in the open market at the currently prevailing price, but, I believe, will.

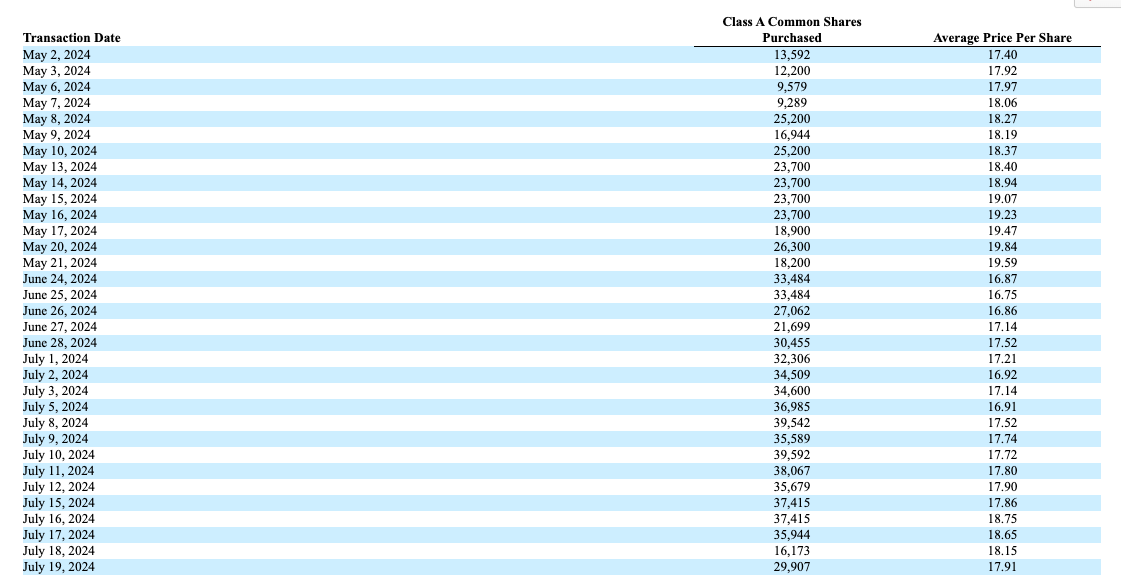

But this argument is perhaps best seen with pictures. The first from a filing on May 23rd, 2024, the second just two months later, from a filing on Jul 23, 2024.

In between the dates there was also a large private transaction between shareholders where they amassed a large proportion of the additional shares. In the interim, they bought the same as the rest of us do, about 25k shares a day in an attempt not to move the stock by their purchases. They appear to be intent on owning this asset and the prodigious, stable, and growing cash flows it produces, but are doing it intelligently.

We look forward to the day where their buying is appreciated and puts upward pressure on the stock, or/and they decide to buy the stub from us at a significant premium.

Finally, in our stable of this could be taken out any day, companies, there’s Openlane (KAR). Openlane operates in an industry replete with private players. The largest operator, Manheim is owned by Cox Enterprises, the largest digital player - although is is moving towards an omni-channel strategy, ACV Auctions (ACVA) was until fairly recently, private.

Like PetIQ, this is a company with industry tailwinds that should continue unabated for the next 3-5 years. It has de minimis capital expenditure needs moving forward, no real reason to access the capital markets that wouldn’t exist if private, plenty of free cash flow, and a very lightly levered balance sheet. The Company has done a lot of the operational heavy lifting that previously held it back, but is necessary to be able to innovate and compete on features for its customers. Finally, it is an actual honest to goodness beneficiary of using AI today by using it to facilitate and expand the capability of its inspections - one of its most significant cost centers. With a board and management team that understand the private markets, free cash flow that can service a high level of debt, and a valuation amenable to historical take privates in the industry, we could see a bid for Openlane emerging sooner rather than later.

As always please feel free to reach out to discuss this or anything else. I think you for your support and will strive to continue to earn your trust.

Basil F. Alsikafi

Portfolio Manager

White Brook Capital, LLC

All investments involve risk, including loss of principal. This document provides information not intended to meet objectives or suitability requirements of any specific individual. This information is provided for educational or discussion purposes only and should not be considered investment advice or a solicitation to buy or sell securities. The information contained herein has been drawn from sources which we believe to be reliable; however, its accuracy or completeness is not guaranteed. This report is not to be construed as an offer, solicitation or recommendation to buy or sell any of the securities herein named. We may or may not continue to hold any of the securities mentioned. White Brook Capital LLC and/or their respective officers, directors, partners or employees may from time to time acquire, hold or sell securities named in this report. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable, or that the investment decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein

How many different strategies has GPRE had in the last 10 years? As someone who's had direct investments in that industry, I have never seen a company jump in with both feet after starting with nothing and it turn out even just okay. Yet, GPRE's foray into the business was even worse than I imagined. Last I looked at this company they were promoting a newfangled corn-oil production idea that was going to require lots of CAPEX. Kind of reminds me of that crazy uncle always tinkering with stuff in his garage—but this particular uncle seems to be playing with bigger toys because the explosions have been quite a spectacle. I can honestly say I never thought GPRE would be a profitable investment outside of liquidation strategy. But I've been wrong more than I care to mention.